When Will Nwtflix Hit 400 Again

Netflix, Inc. (NASDAQ:NFLX) has trended lower since reaching an all time high of $423.21 per share in June, but still up 50% YTD in 2018. The stock has pulled back along with the broader market amid current volatility and concerns raised regarding the company's heavy content spending that is expected to pressure margins leading to recurring negative free cash flow. Shares are now down 35% from its highs which I believe offers a compelling buying opportunity with the company's long term growth story not only intact; but strengthened over the period.

Netflix, Inc. Daily Stock Chart. Source: Finviz.com

Netflix, Inc. Daily Stock Chart. Source: Finviz.com

I'm taking a stand here at $276. On a trailing P/E basis, Netflix is trading at 100x earnings which is the cheapest since Q1 2015. My price target of $400 per share represents a 95x multiple on 2019 earnings. If there is any stock that deserves this type of valuation premium; give it to Netflix. The company has the right combination of unique global scale and unmatched long term growth potential. There are few companies where investors can say with confidence that revenues will double over any period. Netflix is on track to possibly triple revenues in just the next five years at an even higher profit margin.

This article will explore my bullish thesis including a 10-year revenue forecast I developed. The following points will be discussed:

- Company is still in early stage of international growth.

- New focus on foreign language original programming can drive subscriber growth beyond expectations.

- Management guidance of (~$3 billion) in negative free cash flow for 2019 in context represents a 2019 monthly rate of only $1.45 per-subscriber; easily recovered by eventual higher average pricing in my opinion.

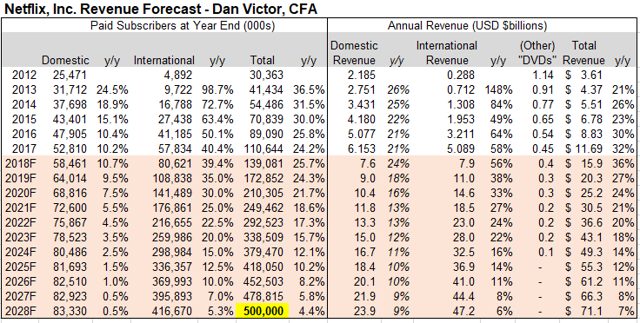

Netflix reaching 500 million subscribers in 10 years might be a conservative estimate.

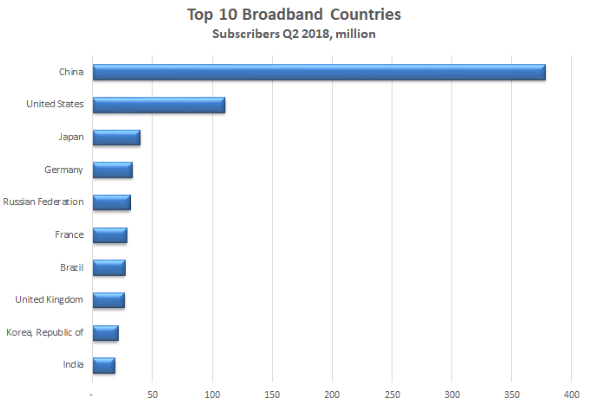

The addressable market for Netflix comes down to broadband access. This month the consultancy firm Point Topic released a report showing there are 1 billion fixed broadband subscribers in the world. Globally excluding China (where Netflix does not operate and instead only licenses its content), I estimate Netflix's current addressable market at around 600 million potential customers. ~500 million outside the United States.

Country ranking by broadband subscribers in Q2 2018. Source – Point Topic.

Country ranking by broadband subscribers in Q2 2018. Source – Point Topic.

For Q3, Netflix reported 73.5 million subscribers internationally or roughly a 14.7% of penetration outside the U.S. By comparison Netflix reported 57 million subscribers in the U.S. relative to 103 million households with broadband, about 55% penetration domestically.

- Focusing only on fixed broadband users worldwide supersedes any consideration of income levels or purchasing power. Presumably; if someone can afford high-speed internet at home (where it's often more expensive in USD terms in developing countries), they can afford to pay for Netflix. It doesn't matter if the household is a family four in Luxembourg or a bachelor in Botswana, there's something for everyone on Netflix.

Again excluding China; the Point Topic Data suggests fixed broadband users worldwide grew 7.5% last year. On top of this figure, Netflix will benefit from two major tailwinds. 1) Still low penetration on average globally for Netflix. 2) The adoption of fixed broadband, from a slower technology like "dial-up", will accelerate over the next decade as costs come down. All the numbers here should go way up. By 2025 it is expected that 75% of the world population will have internet access, up from ~50% today and average speeds will increase with broadband becoming more affordable. The number fixed broadband households worldwide outside of China will double over the next decade.

Netflix is on track to double revenues by 2021 and may triple it by 2024 from current levels.

I estimate that Netflix can reach 500 million total paid subscribers by 2028, up 3.6x from the current levels. Over the period, U.S. penetration will reach around 75% of broadband households while the International market will approach 40%. The numbers look intimidating but many of my assumptions are all-in-all reasonable considering the current momentum and the expectation of a growing pie. Domestic subscriber growth is set to end 2018 up 11% y/y and international subscribers is growing at a 40% rate.

I recognize that "guesstimating" subscriber growth 10 years out is futile, there are just too many variables. But the point is to provide a reference for what is possible. The other component which may be more important in my opinion of course is pricing and that's where Netflix can pull the proverbial lever to really make a difference.

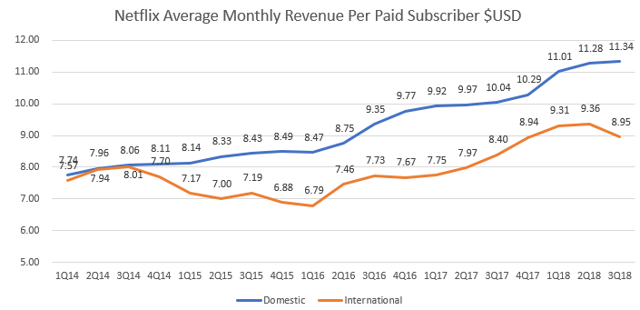

Netflix, Inc. Average Subscriber Revenue. Source: Netflix Q3 2018 Financials

Taking quarterly revenues over the number of paid subscribers we can see trends in average revenue per subscriber between the domestic and international market. I divide the quarterly number by three to get an average monthly rate corresponding the the pricing plans. In Q3 the average subscriber in the U.S. paid $11.34 per month and $8.95 internationally. The Tech consulting firm Comparitech has a report that highlights the different prices Netflix charges by country. In summary the monthly rate in USD varies from a low $3.27 in Turkey to as high $12.37 in Denmark. Apparently the differences are not only related to purchasing power parity; in Japan for example, subscribers pay $5.80 a month according to the report.

- I see these ranges as an opportunity for further upside in average revenue per subscriber. In the U.S., the rate has grown an average 8% per year since 2012, which has been based on the subscription plan mix and the two recent price hikes for the most popular plan.

Domestically, the average rate of $11.34 in Q3 is above the rate of the most popular $10.99/month plan because there are also a growing number of subscribers paying $13.99 for the 4K video option. In the U.S. Netflix has officially hiked the price of its most popular plan twice; $2.00 in October 2015 to $9.99 per month and again last year in October 2017 to the current rate of $10.99.

- I believe Netflix can and will be more aggressive going forward with its price increases. The original programming (award winning) now becomes a more compelling reason for viewers to stay with the service, drawn to the "mega hits".

I predict a price hike of $2 for 2020 to $12.99 for the most popular plan in the US. A $2 price hike could be the answer to reverse currently negative free cash flow. A knock on Netflix is that they spend too much on content, with a budget of $16 billion in 2018. Anecdotally; as a user going through the service I observe some questionable content of varying quality but my view is that for every couple of duds, Netflix has proven to be able to bring out a winner like The Crown, Stranger Things, (or my favorite show 'Ozarks') that can bring in that extra viewer.

Are you watching Foreign language shows?

The same formula for capturing customer retention and pricing power is already being used in the international market at the country level. Management regularly mentions this strategy in its quarterly letter to shareholders.

We continue to expand our international originals, with projects spanning India, Mexico, Spain, Italy, Germany, Brazil, France, Turkey and throughout the Middle East to just name a few. In India, our hit series Sacred Games was followed up by Ghoul in late August. La Casa de las Flores, our latest Mexican original, has become a big hit.

Brazil for example is an interesting case given its large market size and the distinctive Portuguese language. The show 'The Mechanism' by all accounts became a major hit in the country chronicling a sprawling corruption scandal at the highest levels of government. While available to all Netflix subscribers around the world; I'd be surprised if many people outside of Brazil watched the show given the very localized subject matter and politicized story line. This show appears to have been simply made for the Brazilian audience. A show like The Mechanism serves the purpose of becoming must-watch TV for its target audience.

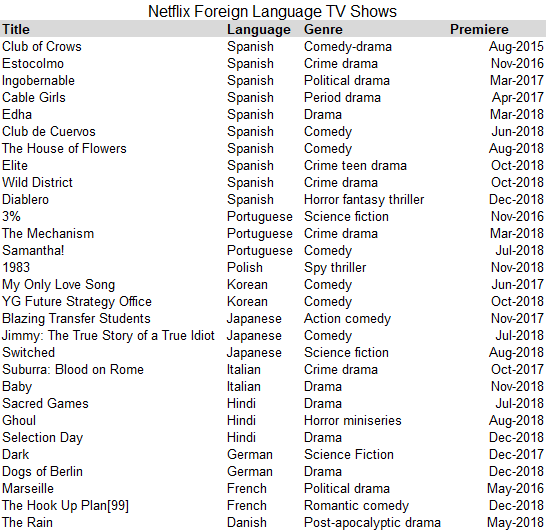

Netflix, Inc. Foreign Language TV Shows. Source: adapted from Wikipedia

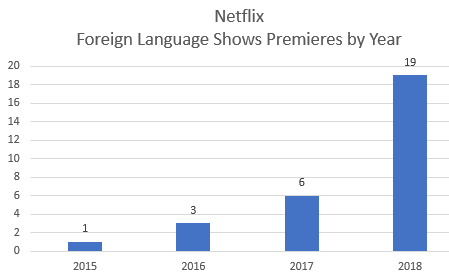

Netflix is moving forward with this model all over the world. The company is premiering 19 foreign language shows in 2018, up from 6 in 2017. Shows in a common language like Spanish can work for many different markets. The potential of getting a big hit in a unique language like Japanese or Danish could help Netflix reach market penetration levels approaching current levels in the US in those markets.

Netflix, Inc. Foreign Language TV Show by Debut Year. Source: Wikipedia

There are also "cross-over" hits, like the Netflix series Narcos in which the live action was 80% in the Spanish language but was a hit in the U.S.. The foreign language shows are crucial to draw viewers in select markets. The assumption is that new subscribers will then stay for the abundance of options and value proposition. Netflix has yet to produce an original foreign language film but continues to secure distribution rights for a growing number of non-English titles to be released as exclusives. Again; in sum this is how Netflix is expanding internationally. There is white space to grow in nearly every country. The market penetration in the US set to reach 60% next year is simply a bar the rest of the world will converge to.

Netflix Revenue Model

Through a combination of continued subscriber growth and price hikes globally; 500 million paid subscribers could translate to $70 billion plus in total revenue in 10 years. My model begins with full year 2018 estimate based on data through Q3 and extrapolates revenue on a per subscriber basis. The summary is below.

- Domestically, subscriber growth slows 120bps in 2019 to 9.5% and trends lower linearly to essentially flat growth of 0.5% y/y by 2027.

- In the International market subscriber growth remains above 20% per year for the next six years and slows to about 5% by year ten.

On the subscriber side, I don't think my estimates will raise any eyebrows in disbelief. The domestic market is becoming saturated and growth railing off into single digits is likely expected my the consensus anyways. International subscribers are set to grow 40% this year and a drop of between 5 and 2.5 percentage points in growth per year for the next decade is reasonable in my opinion.

The key here is the implied revenue per subscriber which is likely more optimistic in my model that current consensus estimates. I see the monthly subscription fee in the US rising to as high as $19.99 per month over the next decade. Price increases in the international market can be much more gradual, below 2% per year, considering the additions will come from more price sensitive consumers in poorer developing countries. Finally, I predict Netflix will end its DVD business in the next 5-6 years.

Netflix, Inc. Revenue Model. Source: Historical from Netflix/ author forecasts

Overall, the confidence here is higher in the near term but even considering consensus estimates of Netflix posting EPS of $6.53 in 2020, the shares today at $280 trade at 42x 2-year-forward earnings. This is cheap for a company that at that time in 2020 would still be expected to increase total revenues above 20% for three to five years out.

Netflix reported a profit margin of 10% in Q3 and 8.5% over the last year. In the next couple of years, I think marketing expenses can be significantly lower leading to higher margins. Right now the company is spending heavily to attract that extra viewer in the US and as part of its early stage global expansion. I believe that "retention marketing" will be much less intensive in the future as the subscriber base matures. On the content side, my view is that Netflix is in the middle of a heavy build-out phase and recurring content spending as a percentage of revenue will begin to decline more significantly as early as 2020.

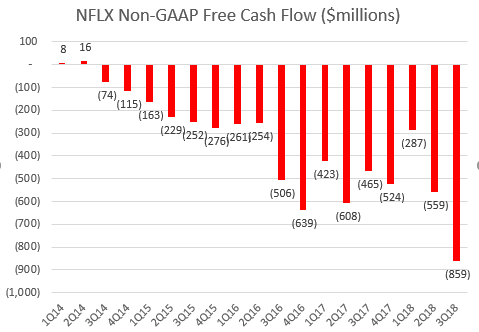

Free Cash Flow is Hiding in Plain Sight

Netflix reported its management version of free cash flow as negative $859.0 million in Q3, -$2.2 billion over the past year and is guiding for -$3 billion for the full year 2018 and 2019.

Netflix, Inc. Quarterly Non-GAAP Free Cash Flow. Source: Netflix IR

I'm not concerned. The content spending makes sense to me and more subscribers are coming. Just for context, $3 billion in negative free cash flow for 2019 translates to about $1.45 per global subscriber per month next year, or $3.91 just including 2019 forecast U.S. subscribers. Netflix could simply hike the price of its most popular monthly plan to $14.99 in the U.S. tomorrow and be free cash flow positive next year. More realistically, a $2 price hike in the U.S. for 2020 and an average $0.50 increase internationally would generated an extra $3 billion in free cash flow.There is little to suggest a mass exodus from the platform due to a marginally higher fee. Still, management right now is more concerned on keeping customers hooked and happy; investors should be OK with that.

Back to valuation

data by yCharts

The last time Netflix was trading at ~100x trailing-twelve-months earnings was Q1 2015. Consensus EPS estimates for 2019 and 2020 suggest earnings are set to grow 60% in each of the next two years. This price-to-earnings growth PEG of 1.6 stands out as making NFLX cheap in my opinion. Among major tech stocks, Netflix PEG of 1.6 compares to Amazon (AMZN) 2.2, Alphabet (GOOGL) 1.8, Microsoft (MSFT) 1.8, Apple (AAPL) 1.6, and Facebook (FB) 1.2. I believe Netflix as a media company deserves a premium here on its growth.

I see a path back to highs around $400 as the market begins the recognize the runway that is being laid for international market growth. I would urge management to be more transparent regarding country by country growth numbers for analysts to better understand the pricing power and upside by market.

In Summary - Netflix is a buy with 45%+ upside in the next year. The company is not going away and brand momentum is only just building internationally. Operating and financial metrics have room to beat expectations in terms of subscriber growth and earnings. Shares deserve a valuation premium to the market. Buy Netflix and Chill.

Author's note: Thanks for reading. I look forward to the comments. If you found value in this article please click the "Like" button. Consider "Following" me to hear about my next stock idea. - Dan

This article was written by

Outside-the-box trade ideas through a powerful multi-sector strategy.

The most extensive coverage on SA! We combine fundamental analysis with a data-driven approach to find "outside the box" ideas.

15 years of professional experience in capital markets and investment management at major financial institutions.

Check out our private marketplace newsletter service *Conviction Dossier* for curated trade ideas.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in NFLX over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: https://seekingalpha.com/article/4216944-buy-netflix-and-chill-going-back-to-400

0 Response to "When Will Nwtflix Hit 400 Again"

Post a Comment